RBL Bank · 0→1 Product Design · 2022

When money is involved,

When money is involved,

trust becomes the product.

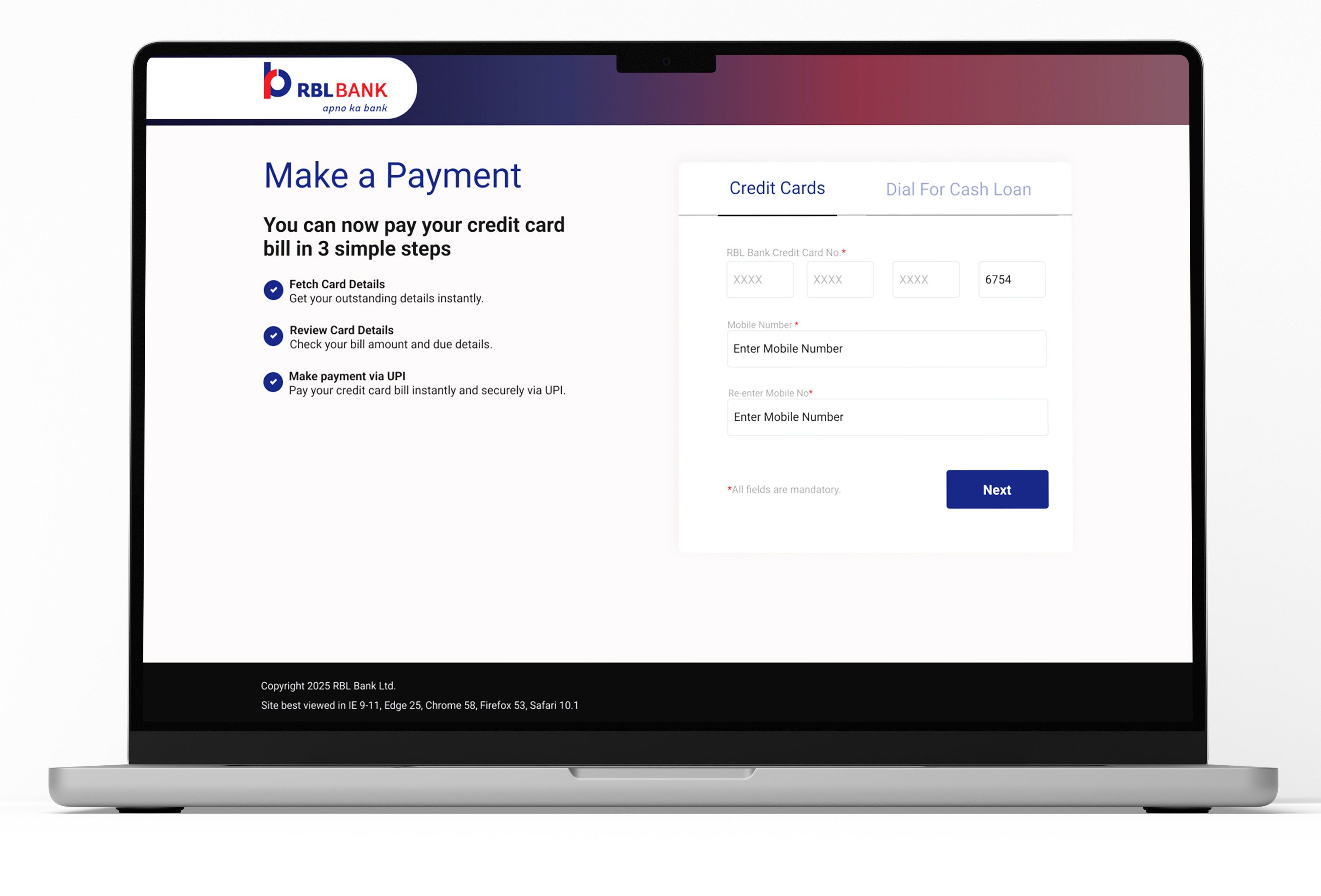

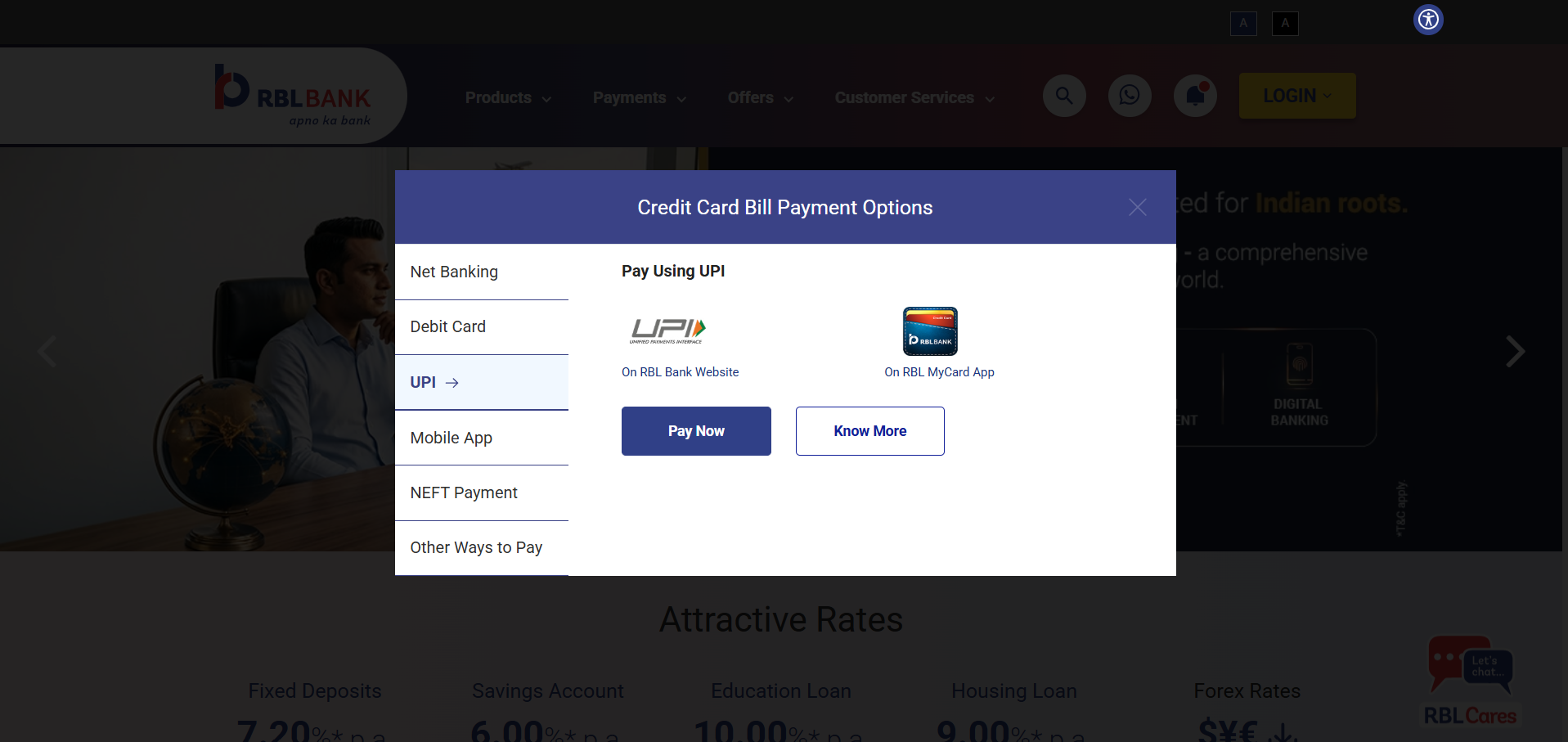

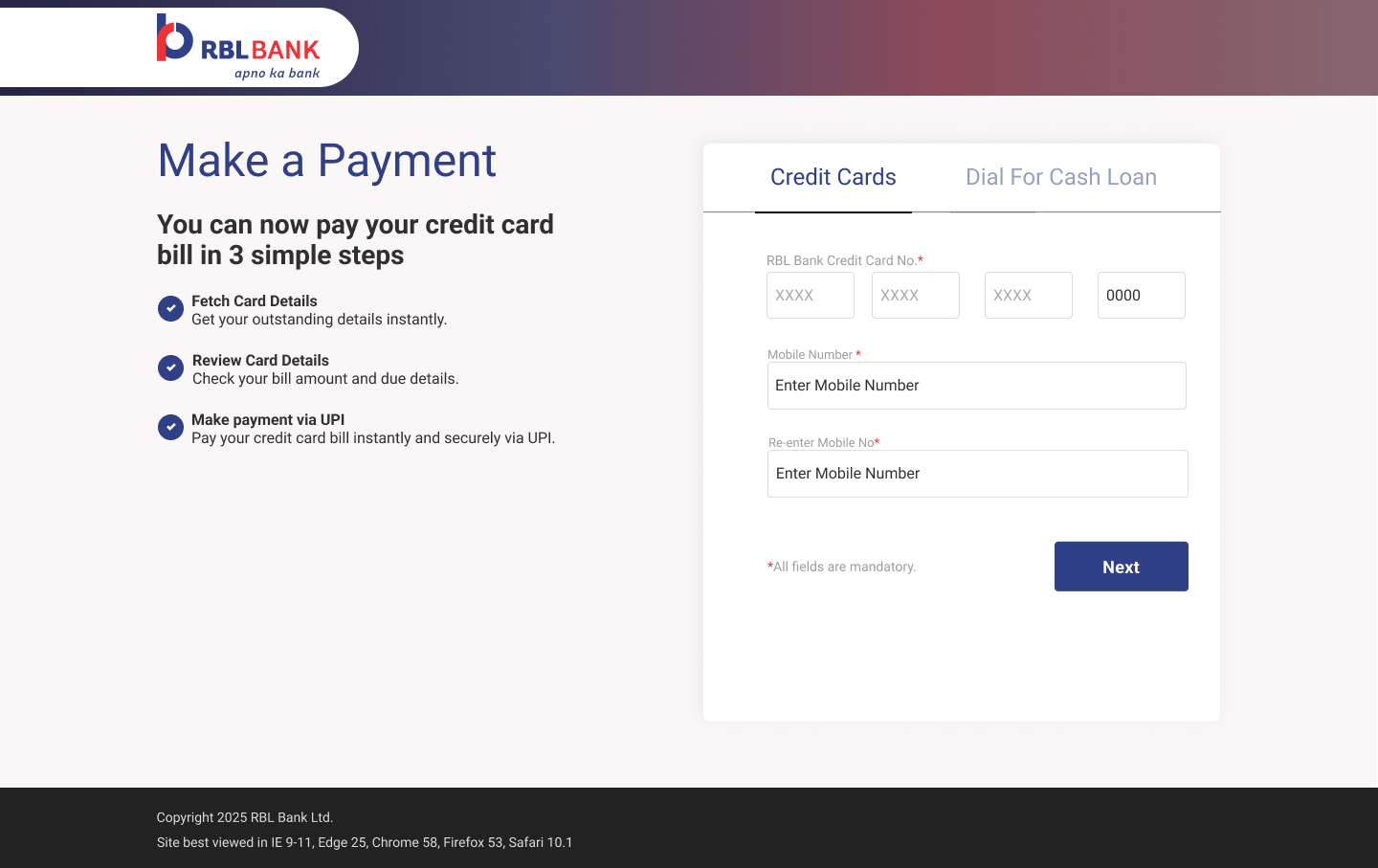

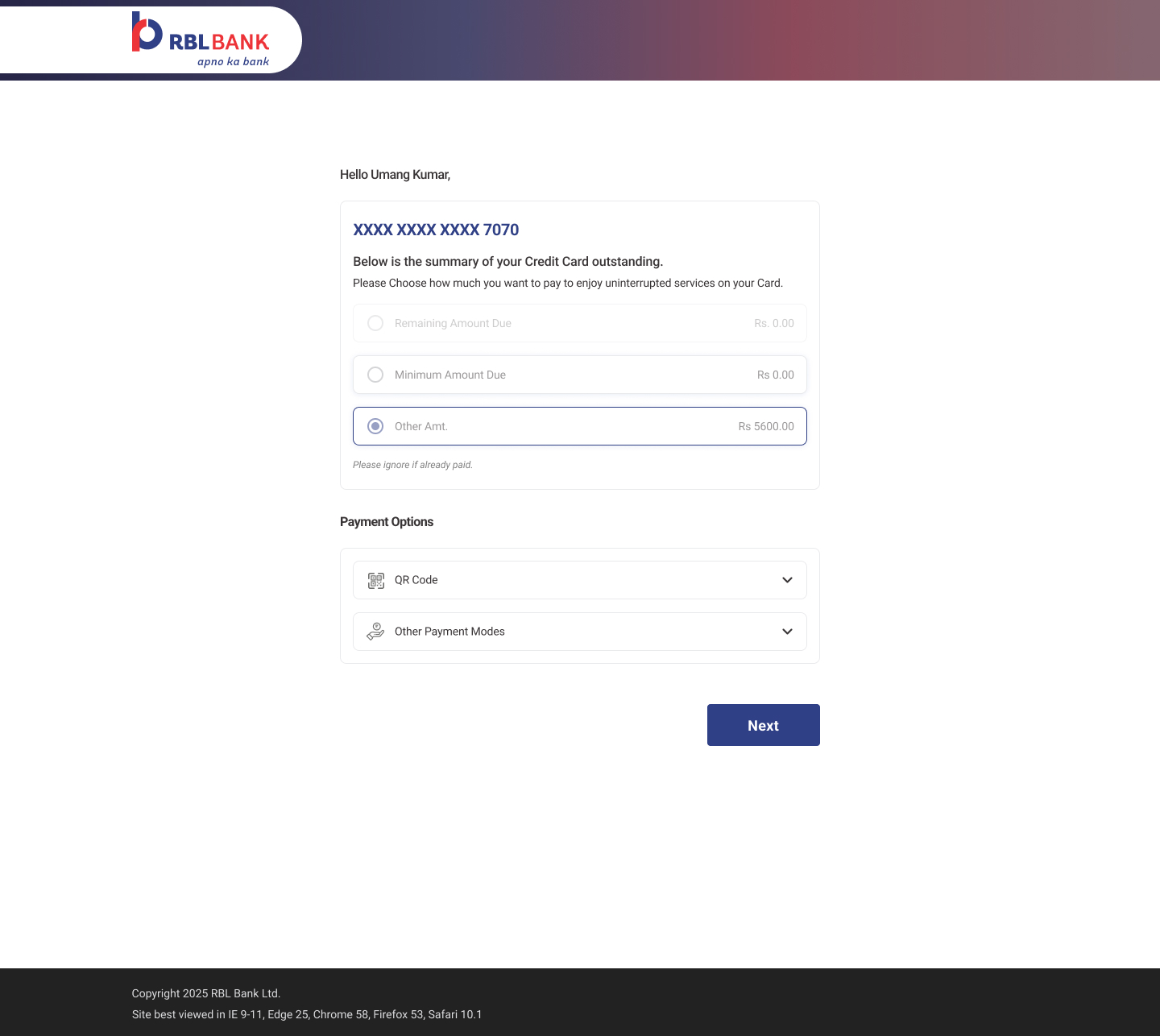

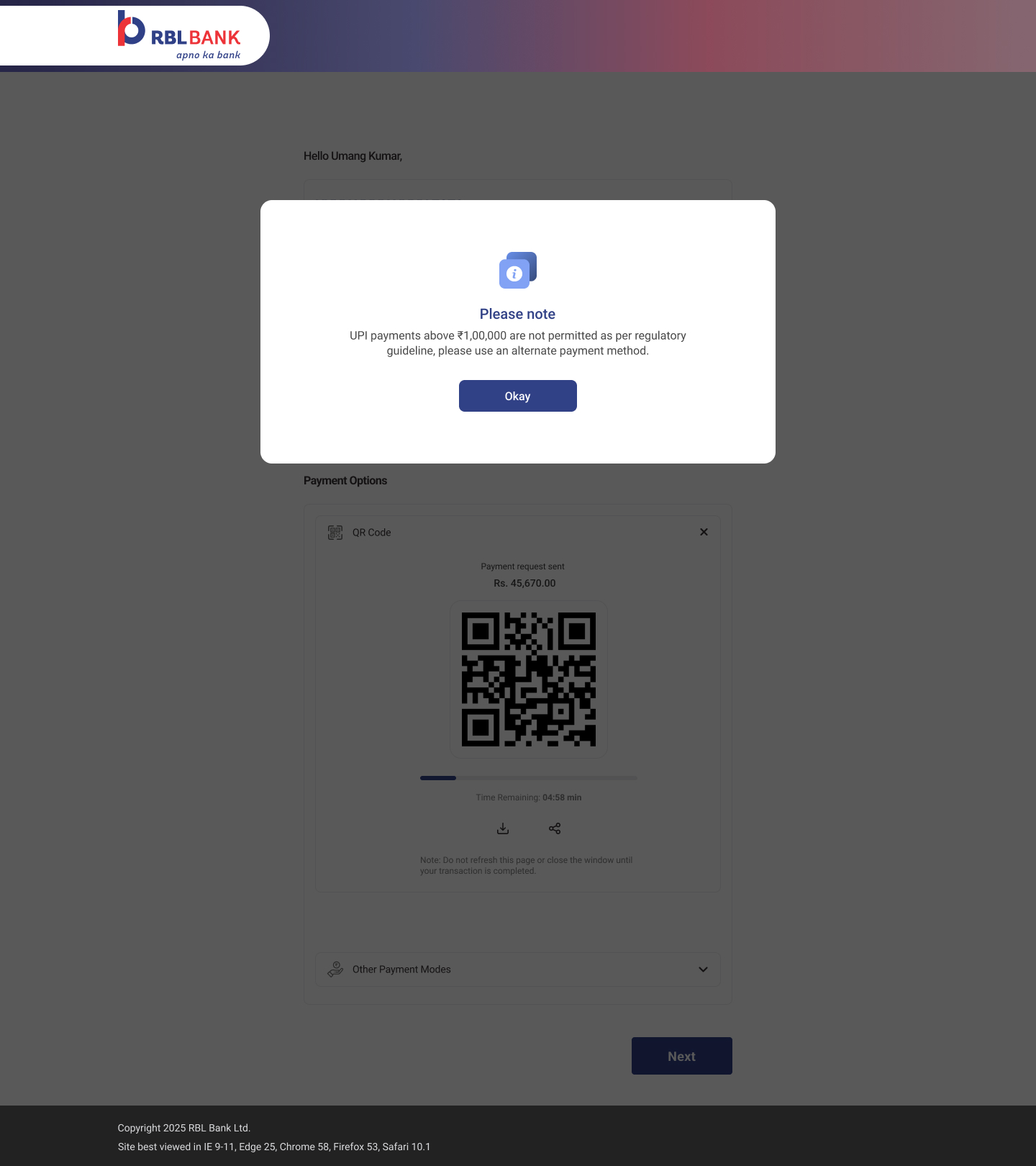

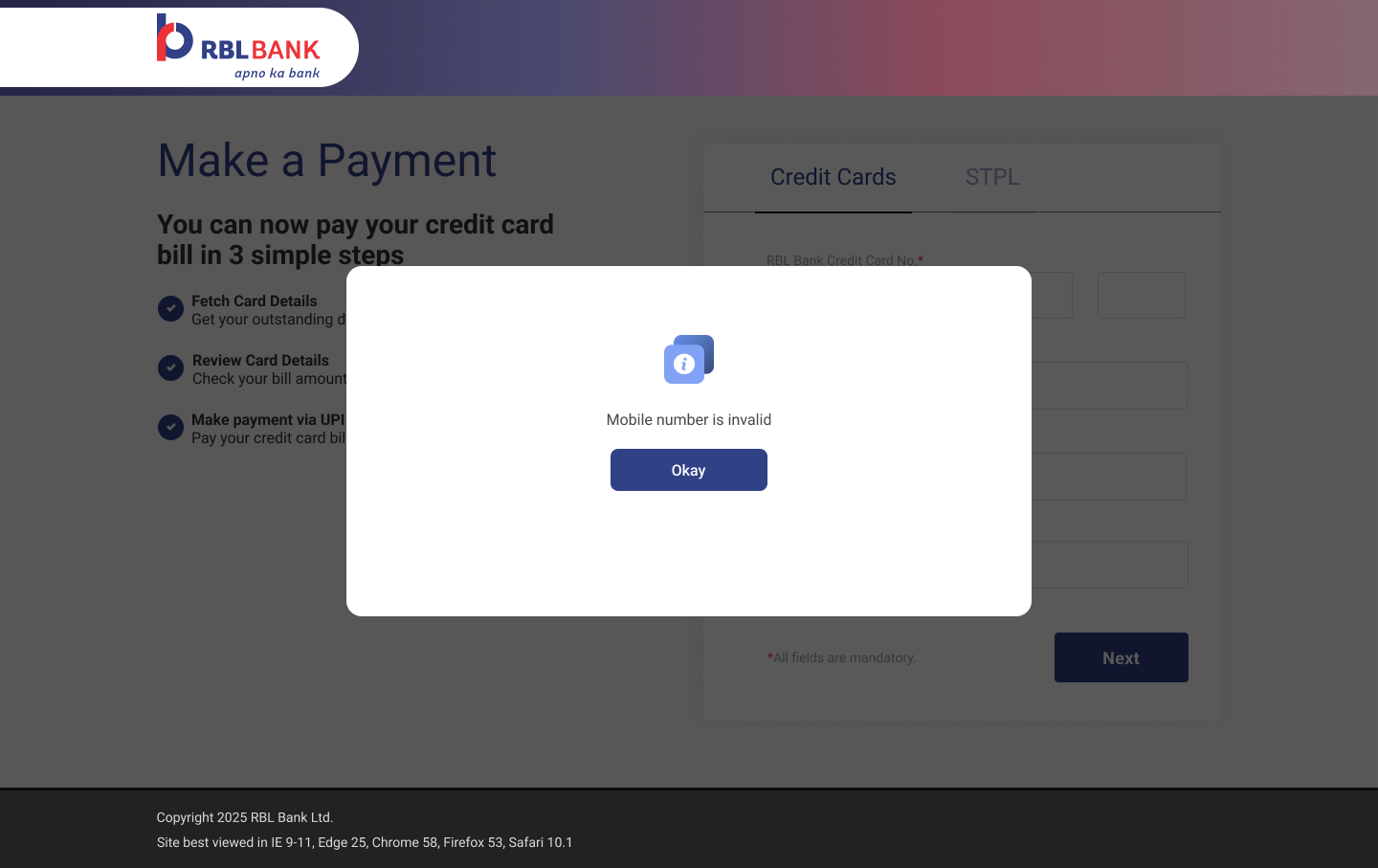

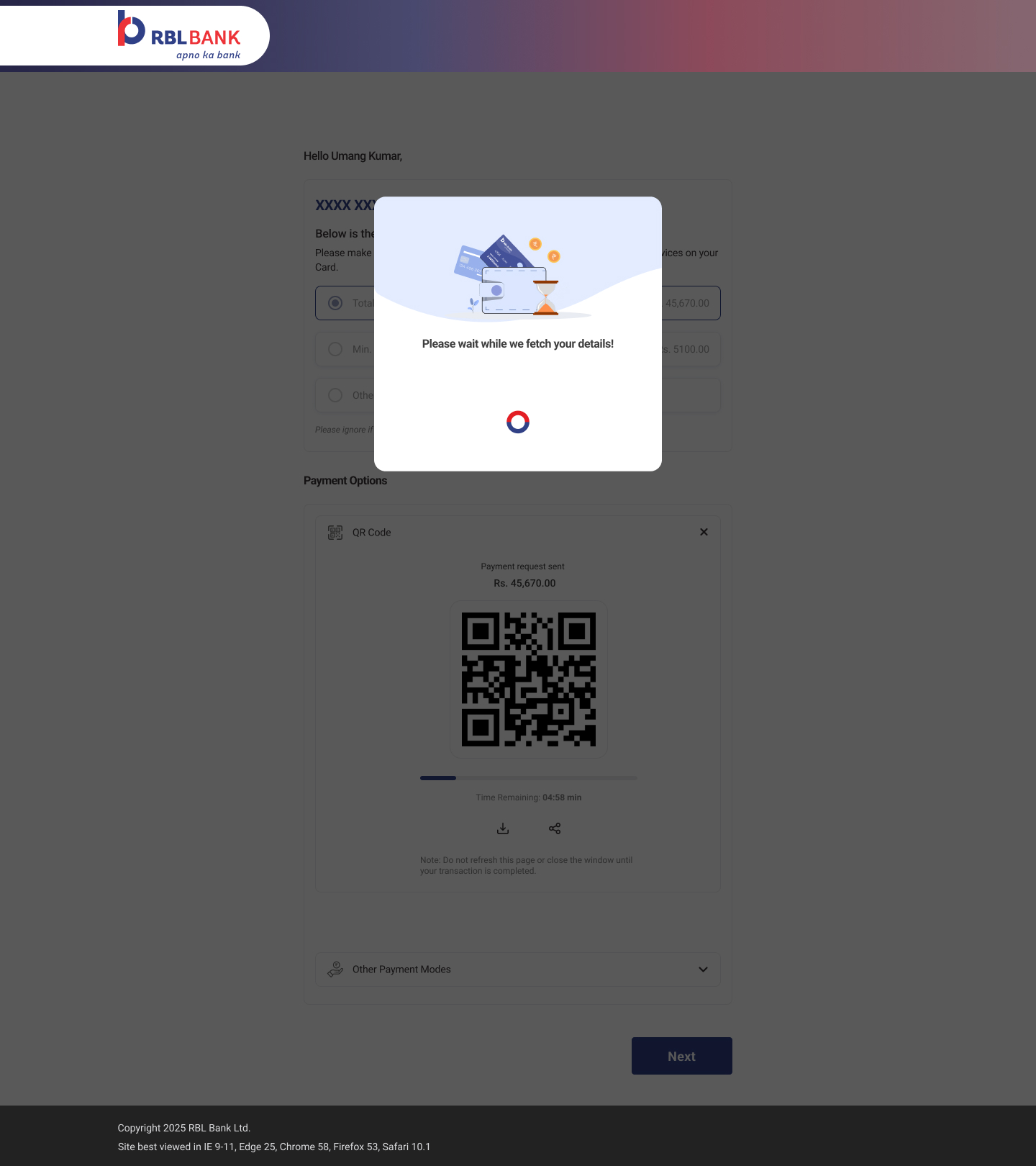

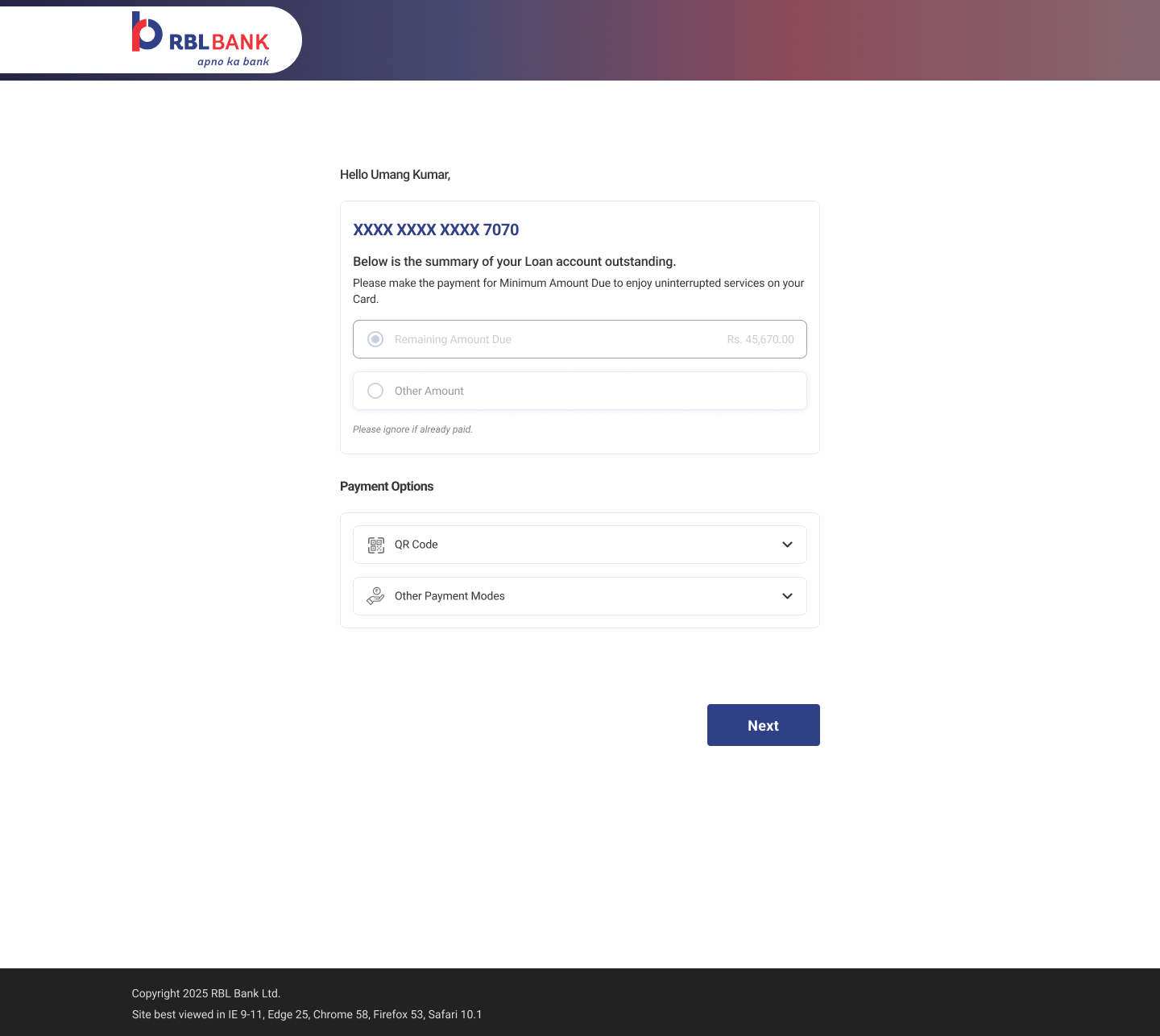

RBL Bank wanted to launch its first UPI-powered credit card payment experience. My challenge was designing a journey customers could trust from the very first transaction — on a platform that had never offered this capability before.

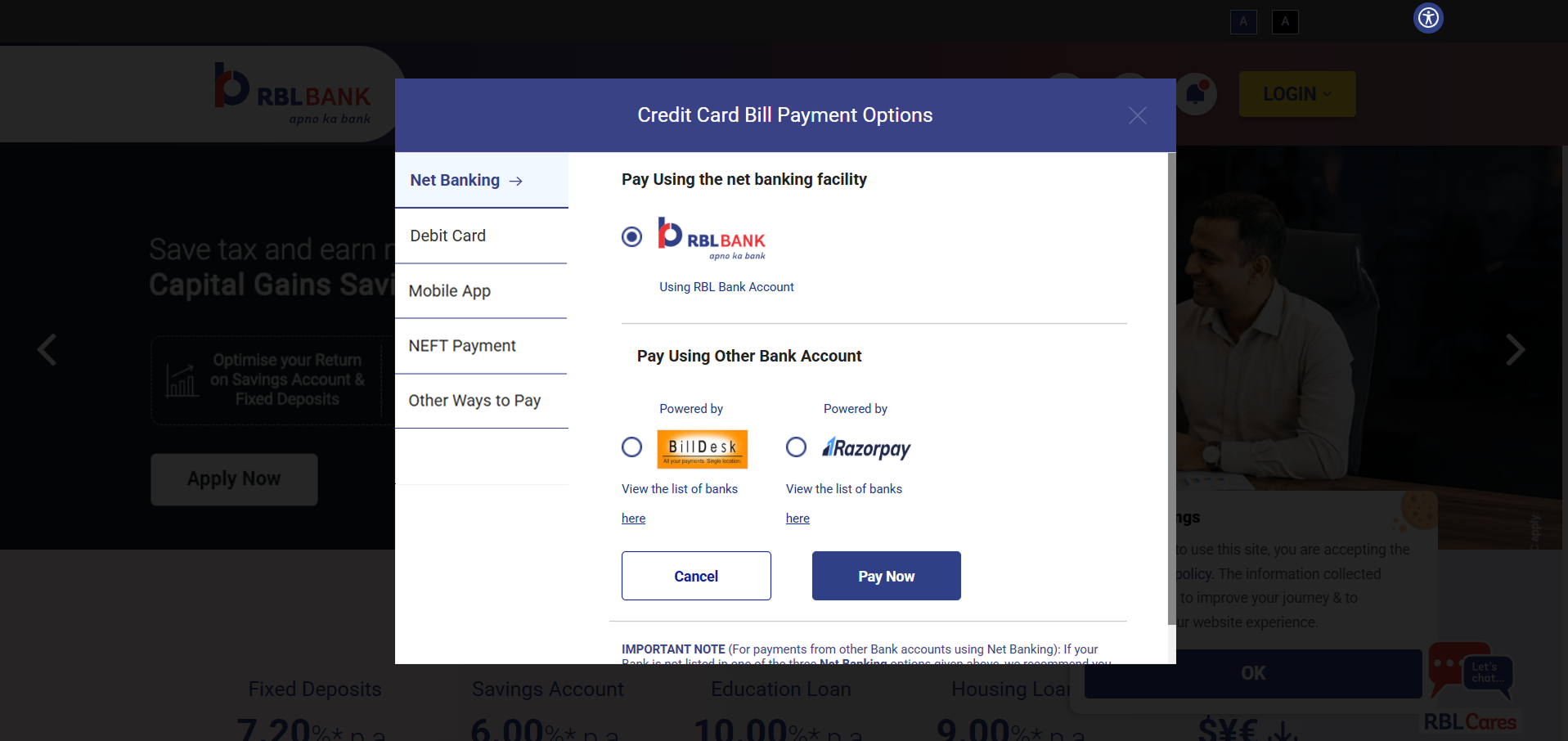

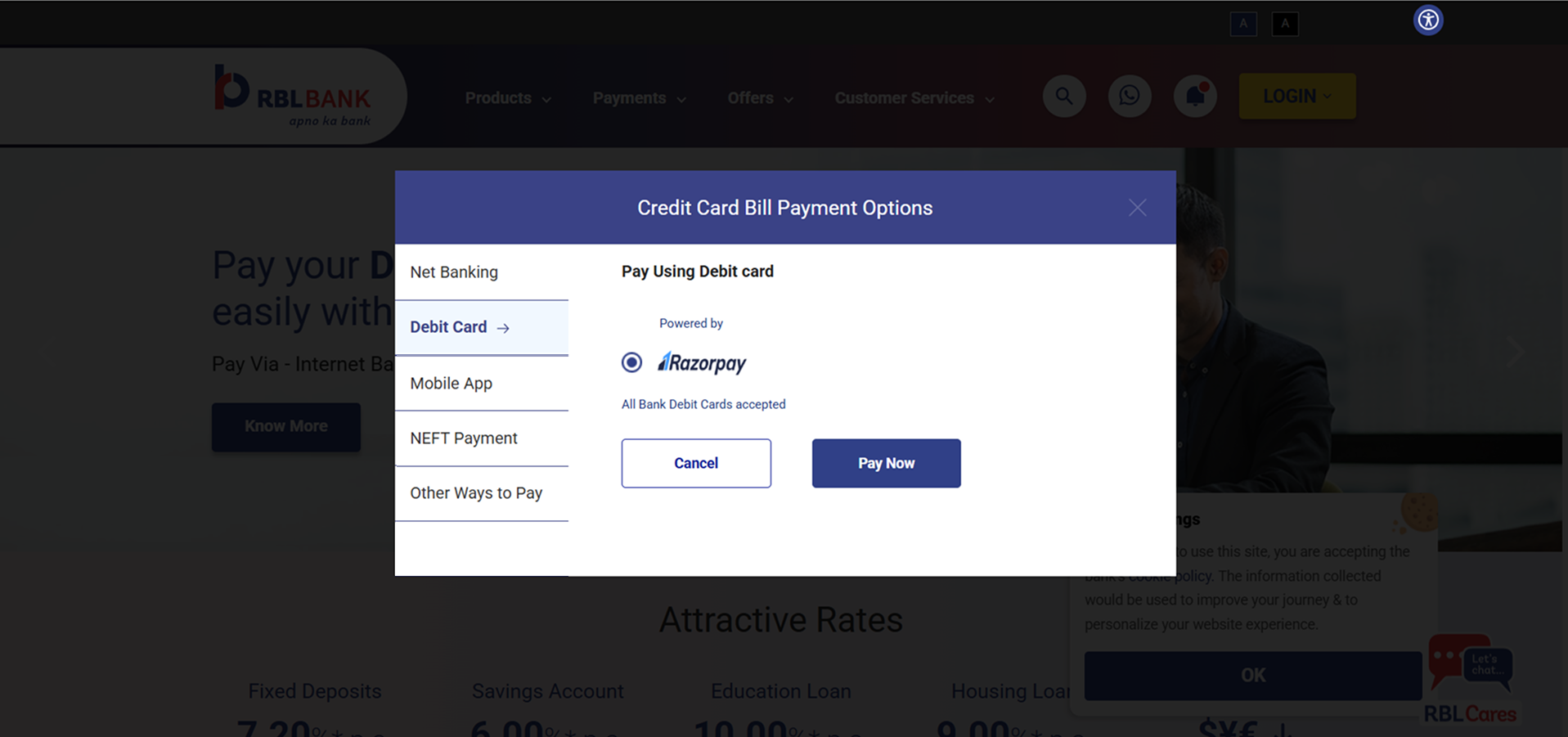

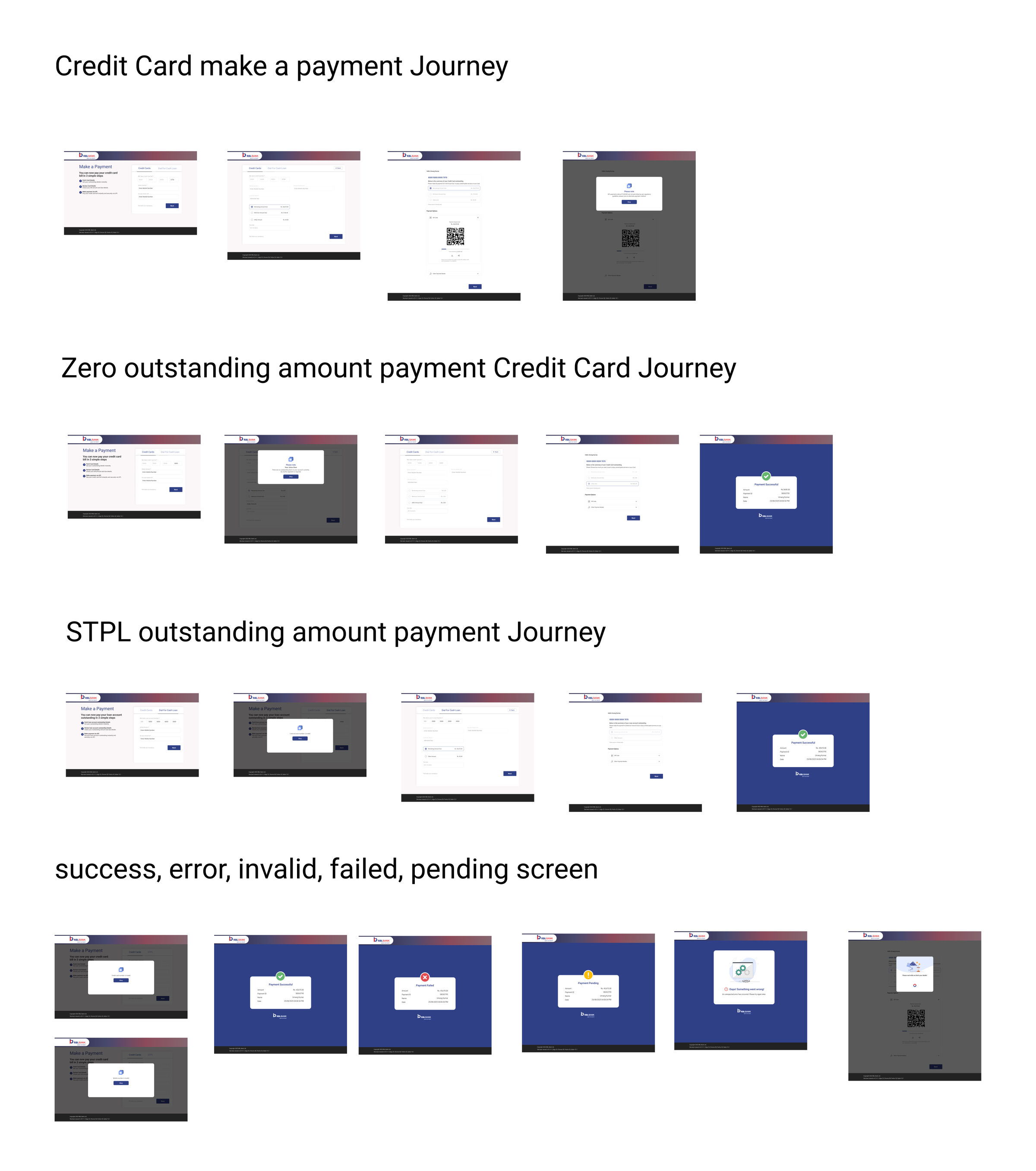

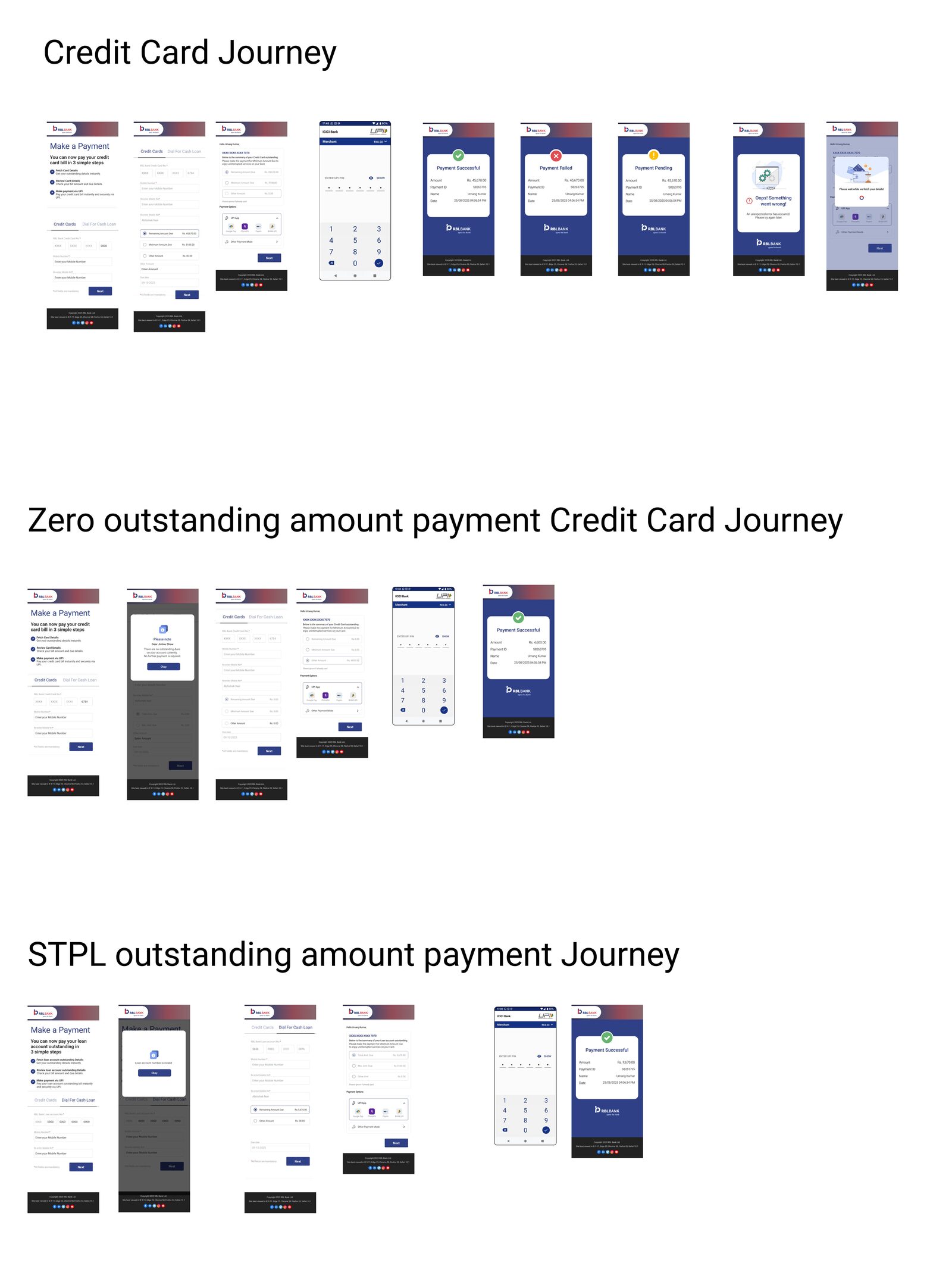

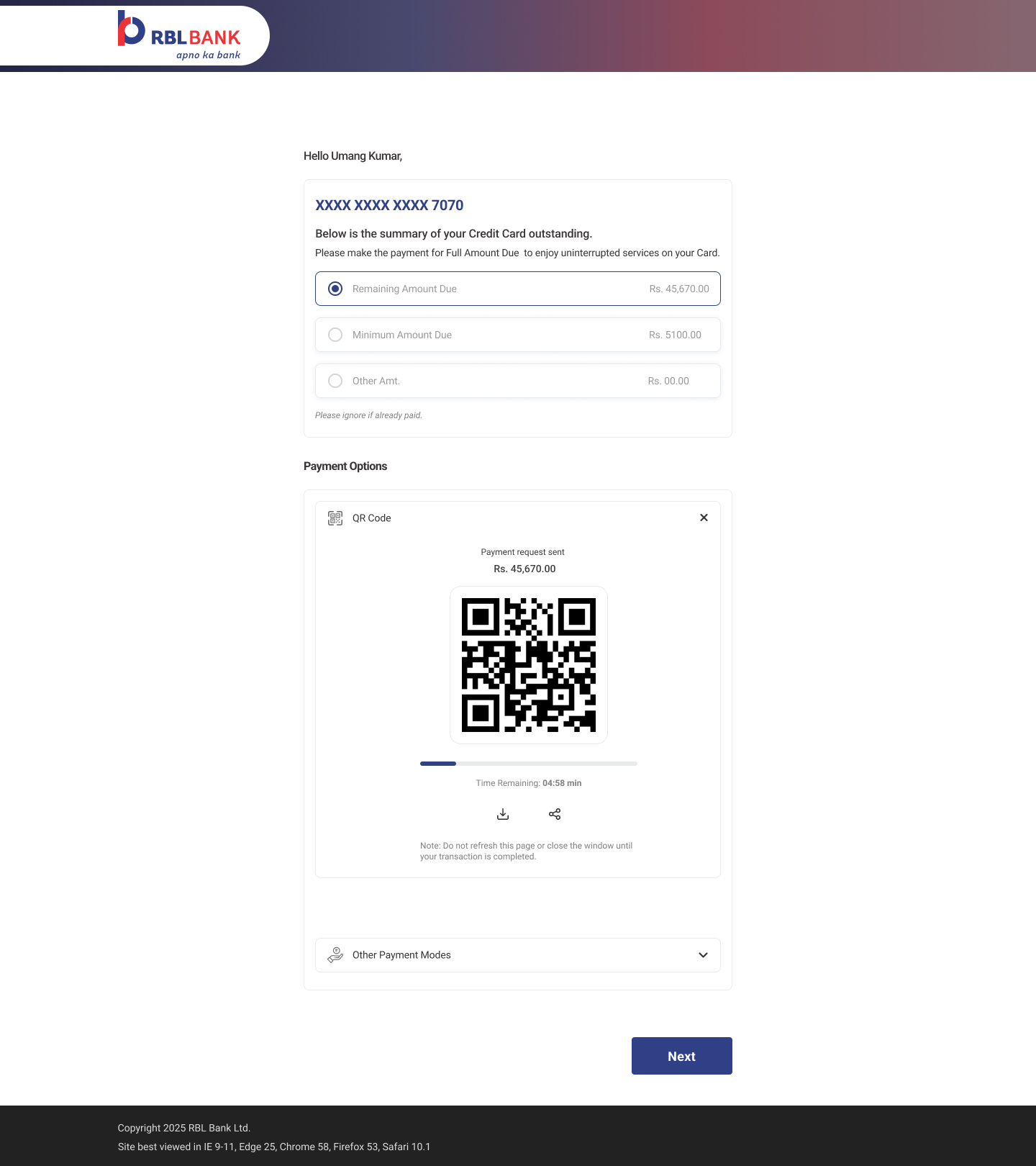

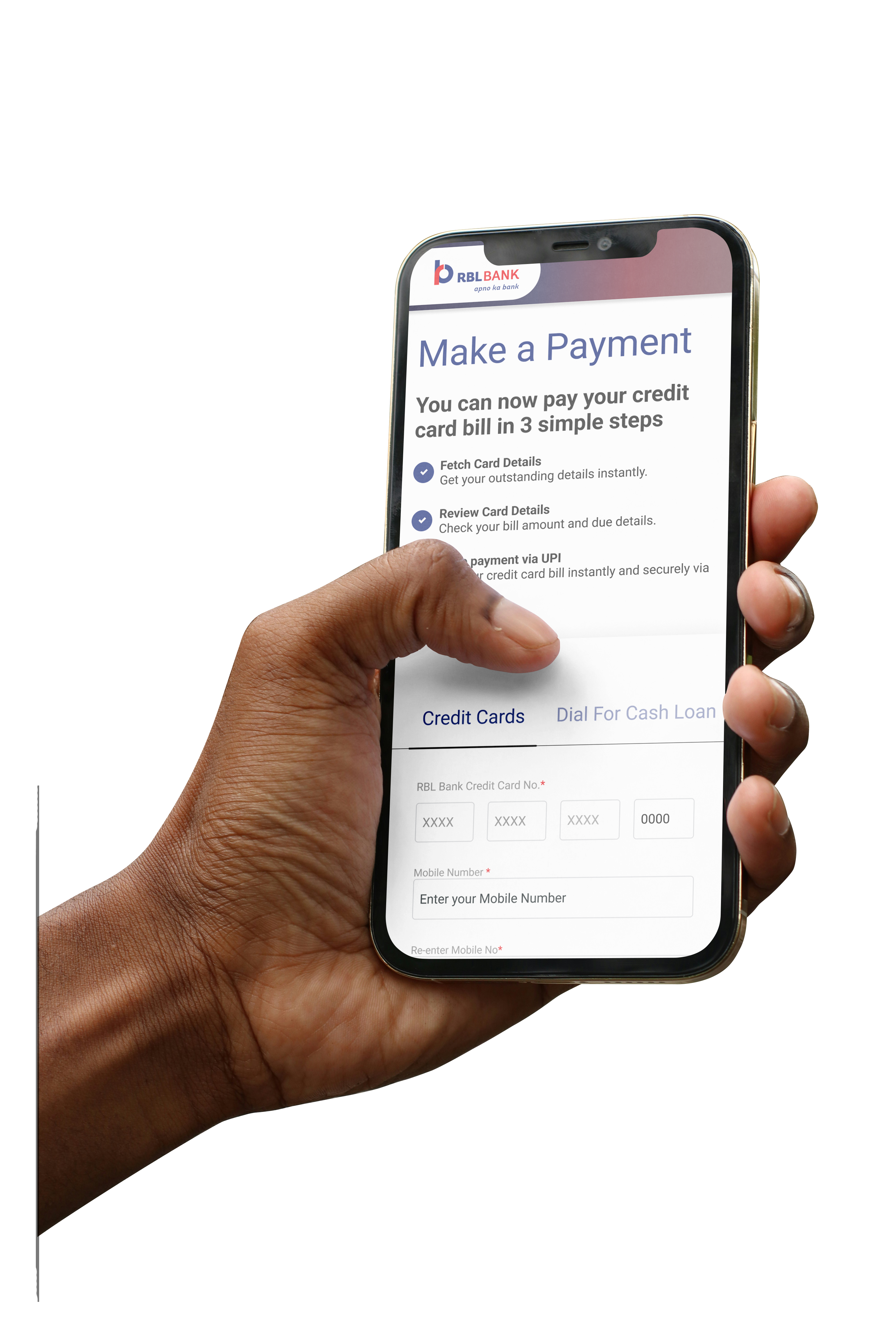

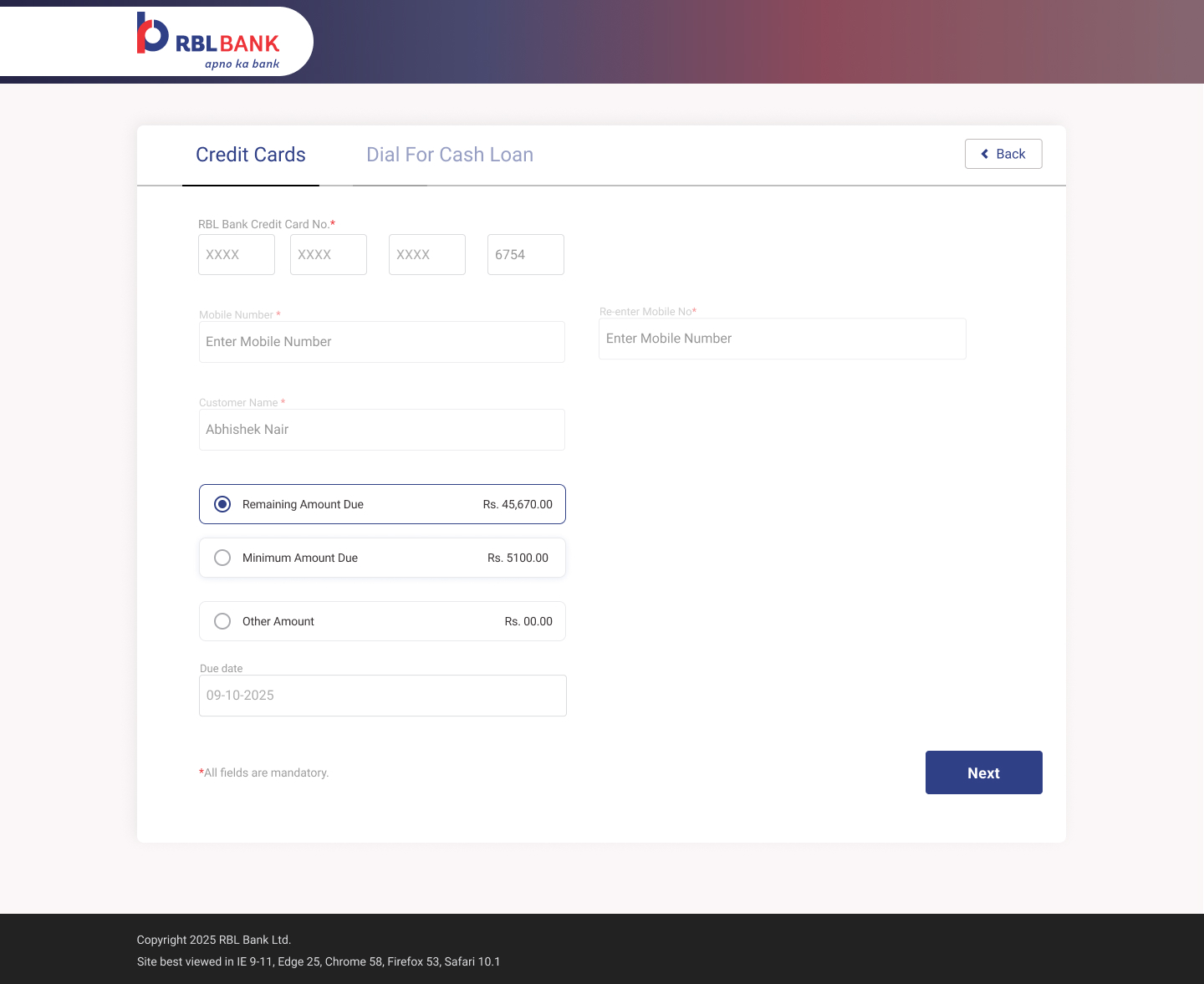

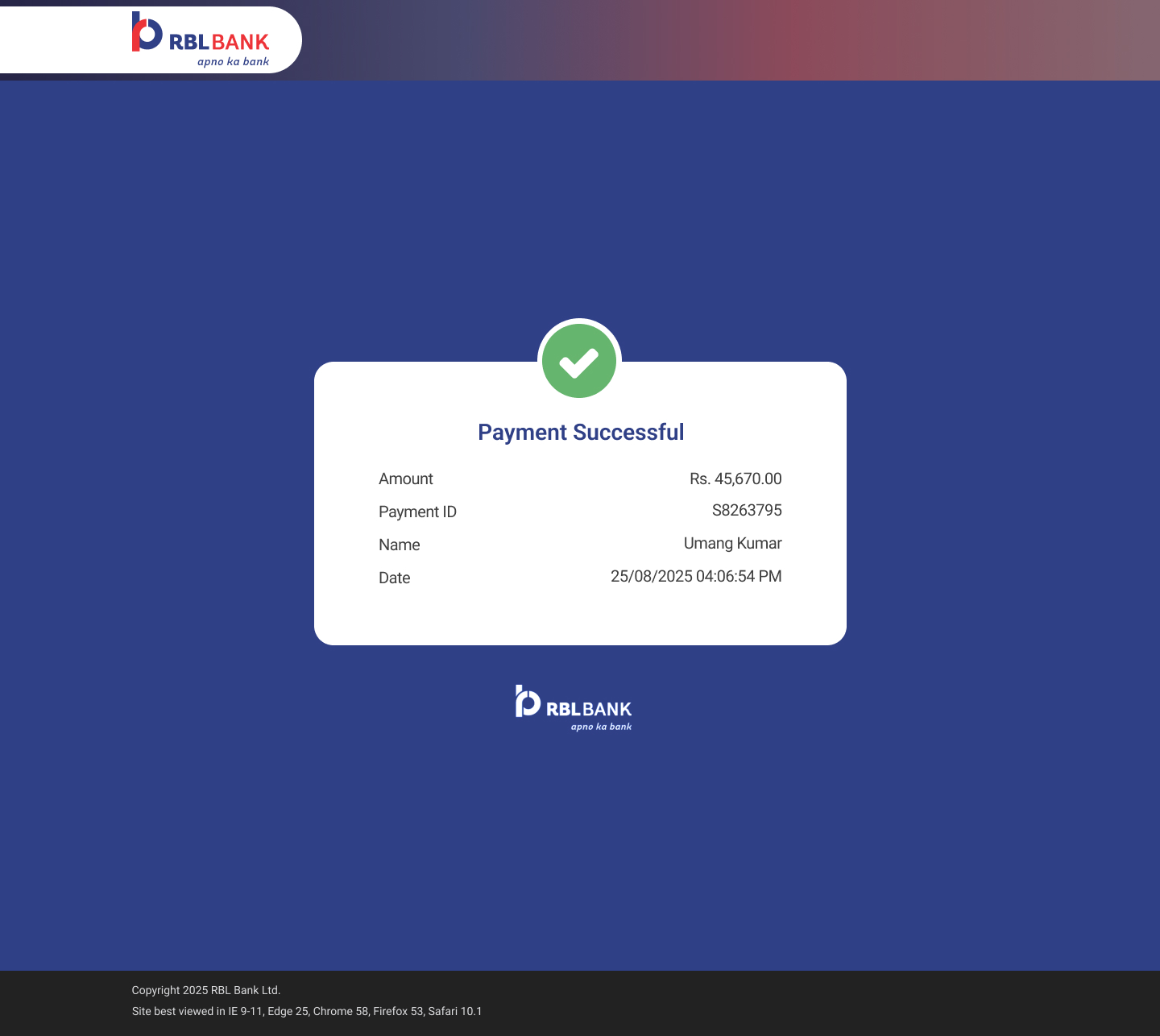

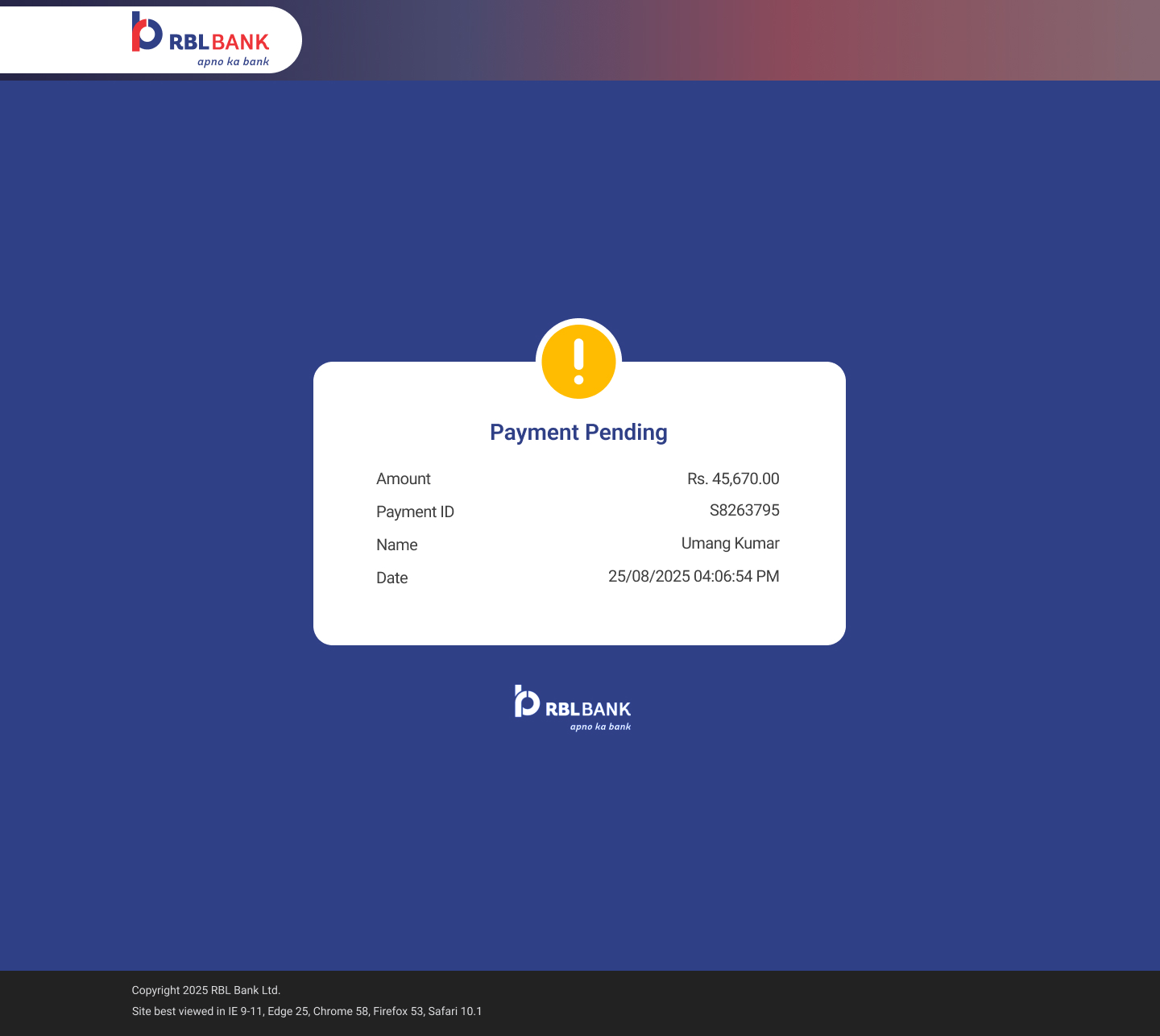

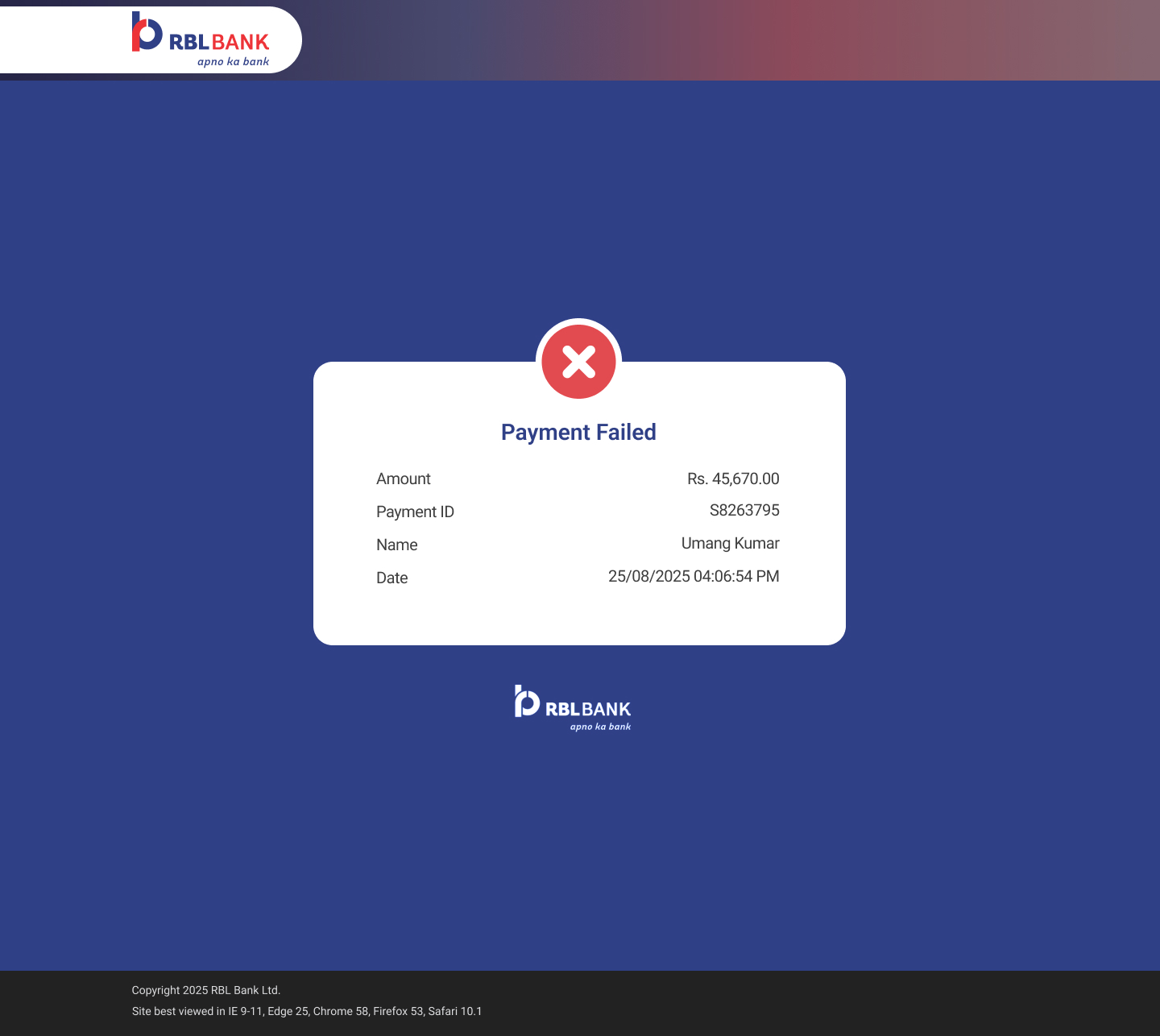

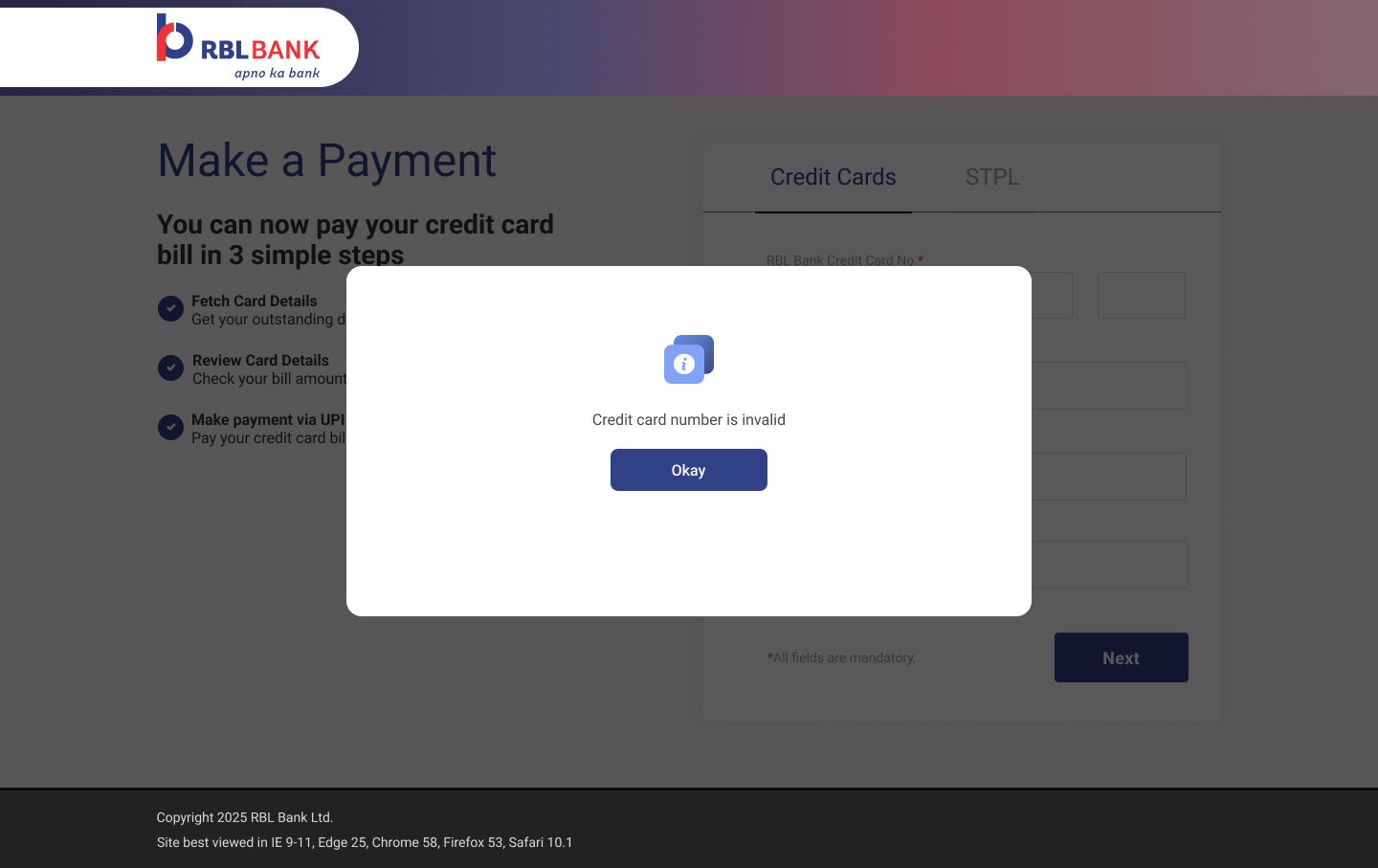

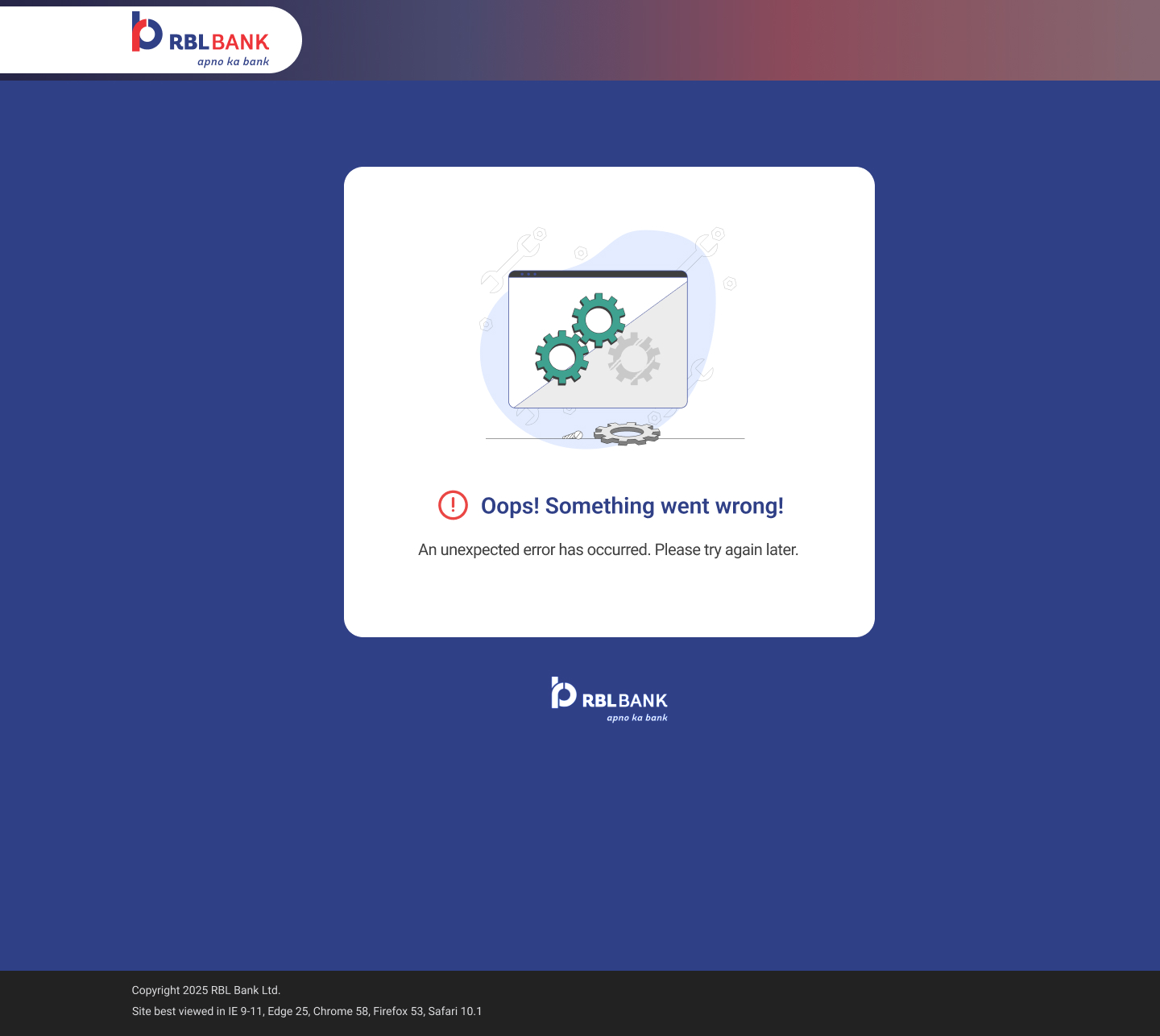

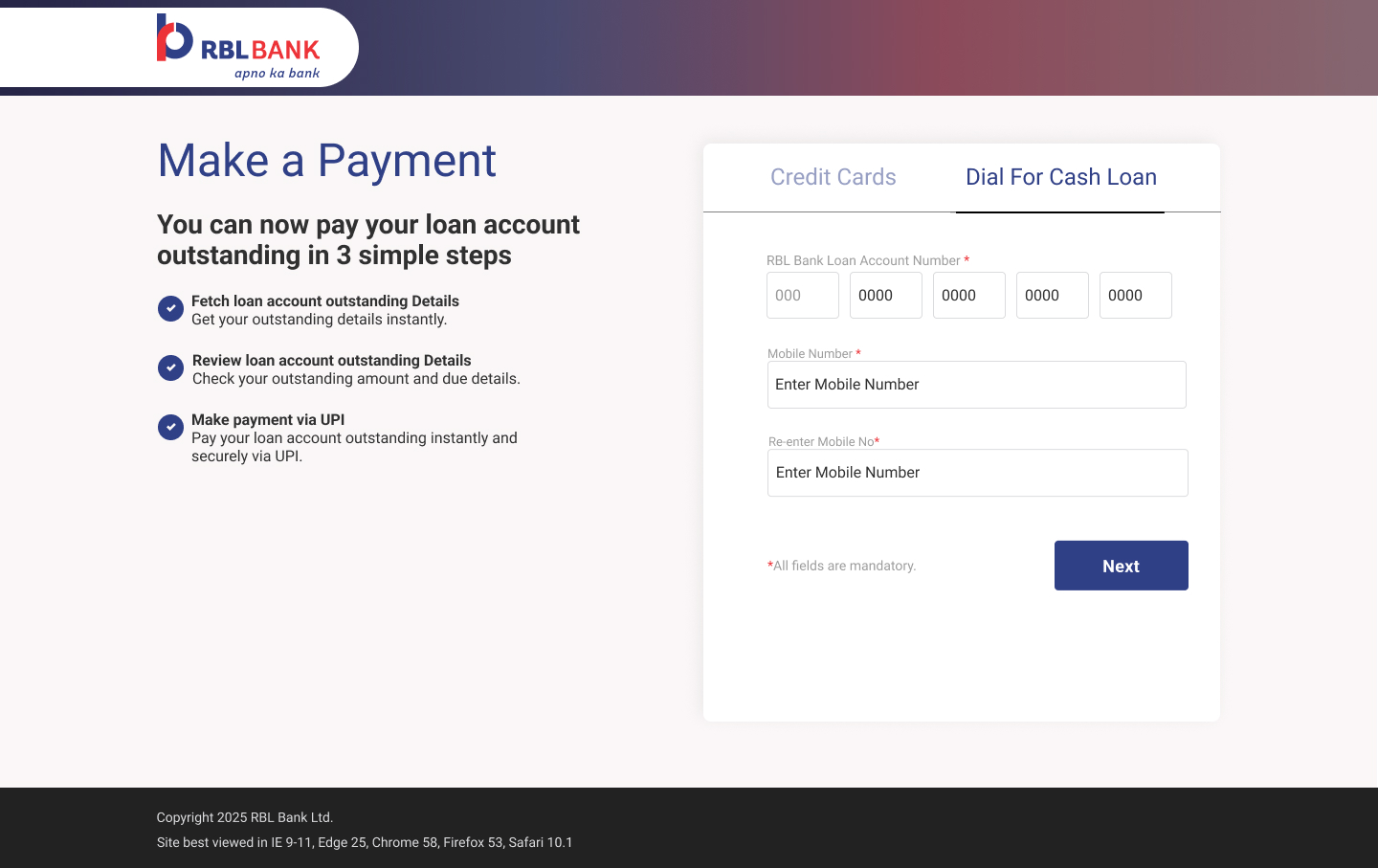

I led end-to-end design of RBL Bank's first UPI payment experience for credit card customers — from blank canvas to shipped product. Before this, customers could only pay their credit card bill online via internet banking or another bank's debit card. UPI wasn't an option. Three distinct payment journeys. Seven-plus edge cases. Every failure state. And one question that had to be answered on every screen: did my money go through?

0→1new UPI capability launched

3complete payment journeys

7+edge cases designed

100%self-service, no agent needed

Design principles

Trust first

Every interaction must build confidence before it builds features

Progressive disclosure

Show only what the user needs at each moment — nothing more

Resilient by design

Edge cases and error states get the same care as the happy path — that's where trust is actually earned

Responsive-first

Mobile and desktop flows designed in parallel, not adapted after

Process

ResearchCompetitive audit · Support log analysis

Insights6 key trust signals identified

Architecture3 journeys mapped and validated

Design & TestingUAT across 3 cycles, 4 defects resolved

LaunchShipped · Self-service UPI live